When I hear the name Irma, I have this vision of someone’s sweet Aunt or Grandmother. And I’m sure there’s a wonderful group of women named Irma that fit into those categories. But today, I’m not going to talk about Irma — I’m going to talk about IRMAA.

IRMAA is the Income Related Monthly Adjustment Amount charged by Social Security on Medicare beneficiaries with higher incomes. IRMAA was first enacted in 2003 as a provision of the Medicare Modernization Act. This provision applied only to high-income enrollees of Medicare Part B. In 2011, IRMAA was expanded under the Affordable Care Act to include high-income enrollees of Medicare Part D as well.

Now, what does this mean. Well, put simply, if your income is over a certain level, you’ll be paying an amount for your Part B and Part D coverage that’s higher than the normal rates for these two parts of Medicare. And, the more you make, the higher that adjusted amount is.

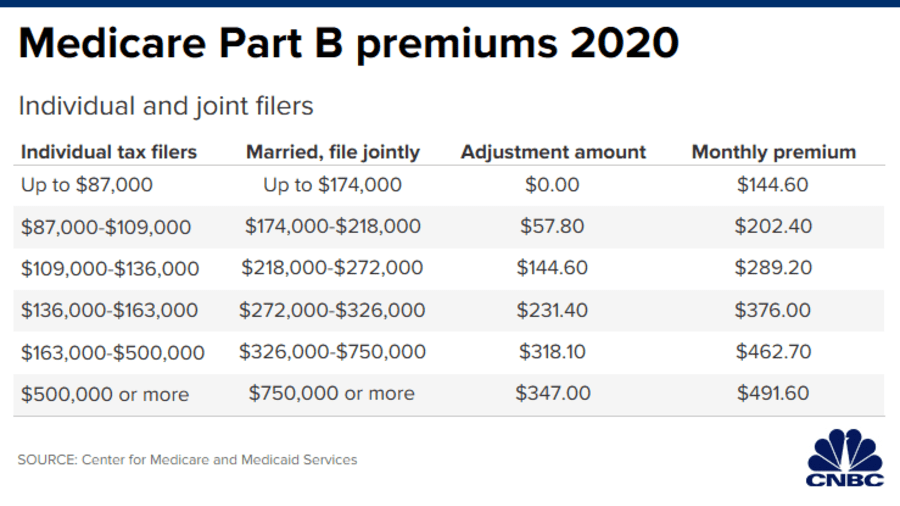

Let’s take a look at Part B which covers medically-necessary services like doctors’ services and tests, outpatient care, home health services, durable medical equipment, and other medical services. Here’s a chart that tells you what the adjusted amounts are by income levels:

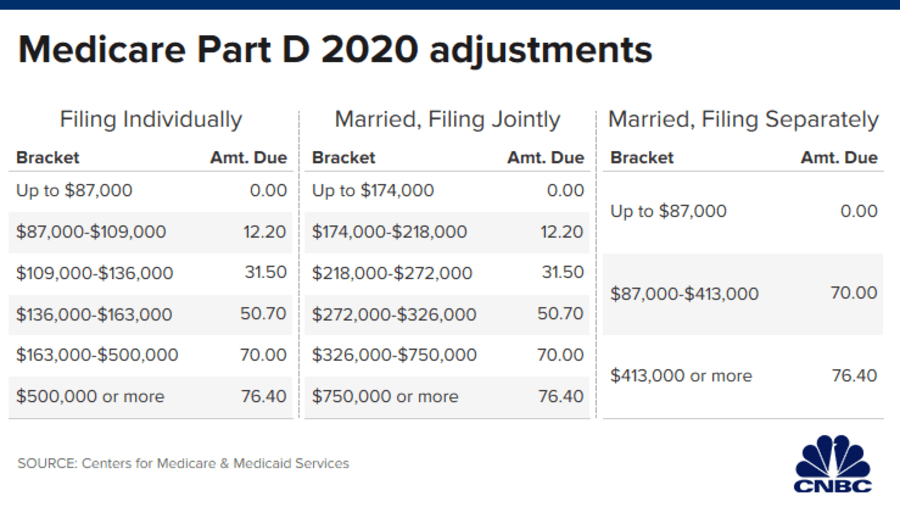

So, if you make up to $87,000 as an individual filer or $174,000 as married, filing jointly, there’s no adjustment for income. And, as you can see from the chart above, as income grows, so does your monthly premium. Now, let’s take a look at Part D prescription drug plans, which also have an IRMAA component.

As you can see from this chart, there’s a comparable increase in premiums as income rises. However, there is a third category here for Married, Filing Separately that we don’t see in Part B. But again, as income rises, so does the monthly cost of your Part D prescription drug plan.

To determine whether IRMAA is applied to your premium, the Social Security Administration looks at the Modified Adjusted Gross Income (MAGI) on your tax return from 2 years earlier. So, if you enroll in Medicare in 2020, the SSA will be looking at your 2018 return. They’ll continue to look back 2 years annually to see if the IRMAA is still appropriate. If your income increases, the IRMAA will increase. If your income decreases, then IRMAA will drop accordingly.

Now, we, as agents, have no control over this. In fact, when we enroll you, we never talk about income. At the time you apply, Medicare will coordinate with SSA and the IRS to get your tax information and make an IRMAA determination. If IRMAA is applied you’ll get a Pre Determination Notice from the Social Security Information. This notice will include:

- That IRMAA will apply,

- What information was used to compute IRMAA,

- What the beneficiary can do if the tax information provided by IRS is wrong,

In addition, this notice will invite you to contact SSA within 10 days if the you believe the information is incorrect before SSA applies IRMAA.

So, if you’re wondering why your friend or relative, who doesn’t make as much money as you do, is paying less for Medicare, now you know!

If you have any questions about Medicare or need any help enrolling, just reach out to me at any time… drop me an email at Marty4Medicare@gmail.com or just click here to download my digital business card and give me a call!

Marty SilbernikAgent, United Insurance Experts